.jpg)

| NSPM in English | |||

Second half of 2011 - Explosion of the Western public debt bubble |

|

|

|

| subota, 25. decembar 2010. | |

|

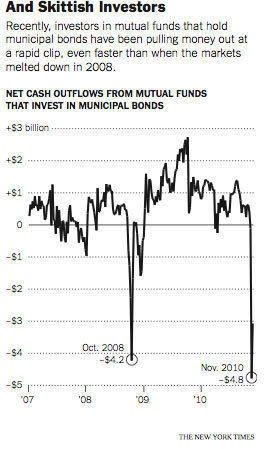

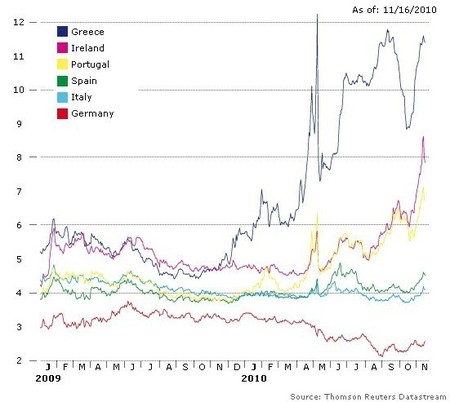

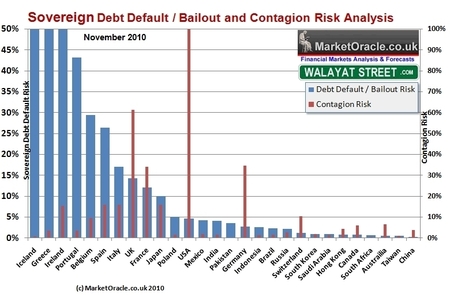

Second half of 2011 - European context and US catalyst - Explosion of the Western public debt bubble The second half of 2011 will mark the point in time when all the world’s financial operators will finally understand that the West will not repay in full a significant portion of the loans advanced over the last two decades. For LEAP/E2020 it is, in effect, around October 2011, due to the plunge of a large number of US cities and states into an inextricable financial situation following the end of the federal funding of their deficits, whilst Europe will face a very significant debt refinancing requirement,[1] that this explosive situation will be fully revealed. Media escalation of the European crisis regarding sovereign debt of Euroland’s peripheral countries will have created the favourable context for such an explosion, of which the US “Muni”[2] market incidentally has just given a foretaste in November 2010 (as our team anticipated last June in GEAB No. 46 ) with a mini-crash that saw all the year’s gains go up in smoke in a few days. This time this crash (including the failure of the monoline reinsurer Ambac[3]) took place discreetly[4] since the Anglo-Saxon media machine[5] succeeded in focusing world attention on a further episode of the fantasy sitcom "The end of the Euro, or the financial remake of Swine fever".[6] Yet the contemporaneous shocks in the United States and Europe make for a very disturbing set-up comparable, according to our team, to the "Bear Stearn " crash which preceded Lehman Brothers’ bankruptcy and the collapse of Wall Street in September 2008 by eight months. But the GEAB readers know very well that major crashes rarely make headlines in the media several months in advance, so false alarms are customary![7]

In this GEAB issue, we therefore anticipate the progression of the terminal crash of Western public debt (in particular US and European debt) as well as ways to protect oneself. Furthermore, we analyze the very important structural consequences of the Wikileaks revelations on the United States’ international influence as well as their interaction with the global consequences of the US Federal Reserve’s QE II programme. This GEAB December issue is, of course, the opportunity to assess the validity of our anticipations for 2010, with a of 78% success rate for the year. We also develop strategic advice for Euroland[8] and the United States. And we publish the GEAB-$ index that will now allow us to synthetically follow the progress of US Dollar against major world currencies every month.[9] In this issue, we have chosen to present an excerpt of the forecast on the explosion of the Western public debt bubble. Thus, the Western public debt crisis is growing very rapidly under the pressure of four increasingly strong limitations: - the absence of economic recovery in the United States which strangles all public bodies (including the federal state[10]) accustomed to an easy flow of debt and significant tax revenues in recent decades[11] - the accelerated structural weakening of the United States in monetary, financial as well as diplomatic[12] affairs which reduces their ability to attract world savings[13] - the global drying up of sources of cheap finance, which precipitates the crisis of excessive debt in Europe’s peripheral countries (in Euroland like Greece, Ireland, Portugal, Spain, ... and the United Kingdom as well[14]) and is starting to touch key countries (USA, Germany, Japan)[15] in a context of very large European debt refinancing in 2011 - the transformation of Euroland into a new "sovereign" that gradually develops new rules for the continent’s public debts. These four constraints generate varying phenomena and reactions in different regions / countries. The European context: the price of the path from laxity to austerity will be partly paid for by investors From the European side, we have thus witnessed the difficult, but ultimately incredibly fast, transformation of the Eurozone into a sort of semi-state entity, Euroland. The delays in the process weren’t only due to the poor quality of the political individuals concerned[16] as the interviews of the "forerunners" such as Helmut Schmidt, Valéry Giscard d'Estaing or Jacques Delors hammered on at length. They themselves never having had to face a historic crisis of this magnitude, a little modesty would have done them good. These delays are equally due to the fact that current developments in the Eurozone are on a huge political scale[17] and conducted without any democratic political mandate: this situation paralyzes the European leaders who consequently spend their time denying that they are really doing what they do, i.e. namely, building a kind of political entity with its own economic, social and fiscal constituent parts, ....[18] Elected before the crisis erupted, they do not know that their voters (and the economic and financial players at the same time) would be largely satisfied with an explanation about the decisions being planned.[19] Because most of major decisions to come are already identifiable, as we analyze in this issue. Finally, it is a fact that the actions of these same leaders are dissected and manipulated by the main media specializing in economic and financial issues, none of which belong to the Eurozone, and all of which are, on the contrary, entrenched in the $ / £ zone where the strengthening of the euro is considered a disaster. This same media very directly contributes to blur the process underway in Euroland[20] even more. However, we can see that this adverse effect decreases because between the "Greek crisis" and the "Irish crisis", the resulting Euro exchange rate volatility has weakened. For our team, in spring 2011, it will become an insignificant event. This only leaves, therefore, the issue of the quality of Euroland’s political personnel which will be profoundly changed beginning in 2012[21] and, more fundamentally, the significant problem of the democratic legitimacy of the tremendous advances in European integration.[22] But in a certain fashion, we can say that by 2012/2013, Euroland will have really established mechanisms which will have allowed it to withstand the shock of the crisis, even if it’s necessary to legitimize their existence retrospectively.[23]

In this regard, what will help accelerate the bursting of the Western public debt bubble, and what will occur concomitantly for its US catalyst, is the understanding by financial operators of what lies behind the "Eurobligations” (or E-Bonds)[24] debate which has begun to be talked about in recent weeks.[25] It is from late 2011 (at the latest) that the merits of this debate will begin to be unveiled within the framework of the preparation for the permanent European Financial Stabilisation Fund.[26] Although, what will suddenly appear for the majority of investors who currently speculate on the exorbitant rates of Greek, Irish,... debt is that Euroland solidarity will not extend to them, especially when the case of Spain, Italy or Belgium will start being posed, whatever European leaders say today.[27] In short, according to LEAP/E2020, we should expect a huge operation of sovereign debt transactions (amid a government debt global crisis) which will offer Euroland guaranteed Eurobligations at very low rates in exchange of national securities at high interest rates with a 30% to 50% discount since, in the meantime, the situation of the entire Western public debt market will have deteriorated. Democratically speaking, the newly elected Euroland leaders[28] (after 2012) will be fully authorized to effect such an operation, of which the major banks (including European ones[29]) will be the first victims. It is highly likely that some privileged sovereign creditors like China, Russia, the oil producing countries,... will be offered preferential treatment. They will not complain since the undertaking will result in their sizeable assets in Euros being guaranteed.

------------- IMPORTANT: The English and German of Franck Biancheri’s book “The World Crisis: The Path to the World afterwards – Europe and the World in the 2010-2020 Decade” are now available. They can be ordered directly from the publishers, Anticipolis Editions (www.anticipolis.eu). - Public announcement GEAB N°50 (December 16, 2010) [1] Worth more than € 1,500 billion per year in 2011 and 2012, including of course the United Kingdom. [2] The US municipal bond market ("Munis") is used to fund the local transportation, health, education and sanitation infrastructure, ... It’s worth nearly 2,800 billion USD. [3] Source: Reuters, 8/11/2010 [4] In a 20.11.2010 article Safehaven tonne indeed openly expressed surprise over the "silence" of the major financial media on the issue. [5] The Financial Times, for example, has for the last month, begun to publish two or three articles per day on its website’s homepage on the so-called "Euro crisis" and to manipulate news, such as the statements of German leaders, to artificially create feelings of anxiety. Finally, even some of the French media are beginning to realize what an incredible political propaganda machine the Financial Times has become, as this recent article by Jean Quatremer in the Libération shows. [6] By way of comparison, no investor has lost money in the "Greek and Irish episodes" of the "Euro crisis", whilst tens of thousands have lost considerable sums in the recent US Muni crash... yet the media covers the first and not the second. [7] LEAP/E2020 would like to remind readers of previous GEAB analyses that the discussion over the "Euro crisis" is of the same order as the Swine fever outbreak a year ago, namely a large-scale manipulation of public opinion to serve two purposes: first, to divert public attention from more serious problems (with Swine fever it was the crisis itself and its socio-economic consequences; with the Euro it is simply to divert attention from the situation in the United States and the United Kingdom), and secondly, to serve the goals of players with a major interest in creating this situation of fear (as regards Swine fever it was pharmaceutical laboratories and other related service providers; as regards the Euro, financial players are earning a fortune by speculating on the public debt of the countries concerned (Greece, Ireland, ...)). But just as the Swine fever crisis ended in a masquerade with governments stuck with colossal stockpiles of now worthless vaccines and masks, the so-called Euro crisis is going to end up with players who will have to redeem their so “profitable” bonds for next to nothing whilst their dollars will continue to fall in value. The summer of 2010 has already shown, however, the direction of events. Source: Bloomberg, 18/11/2010 [8] Following the methodology of political anticipation, in the past years our team has, of course, looked at the possibility that the Euro might disappear or collapse. Its conclusion is cut and dried because we have identified only one set-up where such a development would be feasible: at least two major Eurozone states must be headed by political forces wishing to revive intra-European conflicts. According to our team, this prospect has zero probability of taking place in the next two decades (our maximum anticipation span in political matters). So, exit this scenario, even if it makes some with nostalgia for the Deutschmark and Franc sad..., some economists who believe that reality pays little attention to economic theories, and some Anglo-Saxons who cannot imagine, without pain, a European continent which carves out its economic and financial path without them. According to Wikileaks even Mervyn King, head of the Bank of England, believes in an accelerated integration in the Eurozone as a result of the crisis, which recounts his conversations with US diplomats (source: Telegraph, 6.12.2010). Our work on the Euro therefore focuses on the anticipation of the Eurozone’s laborious journey in adapting to its new status as Euroland in the context of the global systemic crisis. Incidentally, it is worth noting that this orgy of criticism and analysis that essentially the US and especially British media lavish has an undeniable value for Euroland leaders: it throws light on all the obstacles laid along the Eurozone path, a sine qua non for avoiding pitfalls. It's paradoxical, but it's an advantage not enjoyed by British or US leaders ... except when they read the GEAB. [9] And not in relation to “made to measure” currencies as is the case for the Dollar Index. [10] The New York Times has posted a very informative game called "You solve the budget problem" on its website which allows each player to try and restore the state of federal public finances according to its socio-economic priorities and policies. Feel free to put yourself in the shoes of a Washington decision maker in and you will see that only political will is lacking to solve the problem. Source: New York Times, 11/2010 [11] Sources: CNBC, 26.11.2010; Le Temps, 10.12.2010; USAToday, 30.11.2010; New York Times, 4.12.2010 [12] The United States funds its deficits by a huge daily grab of available global savings. The country’s diplomatic credibility and effectiveness are therefore two essential features for its financial survival. But Wikileaks’ recent revelations are very damaging to the credibility of the State Department, whilst the recent complete failure of the new Israeli-Palestinian negotiations illustrates a growing ineffectiveness of US diplomacy, already very sensitive at the last G20 in Seoul. See the more detailed analysis in this issue. Sources: Spiegel, 8.12.2010; YahooNews, 7.12.2010; YahooNews, 8.12.2010 [13] Even Chinese officials consider that the US fiscal situation is markedly worse than Euroland’s. Source: Reuters, 8.12.2010 [14] Iceland, Ireland ... the United Kingdom, the United States, was the accursed follow-on of sovereign insolvency that LEAP/E2020 anticipated more than two years ago. Events are moving slower than we expected, but 2011 risks proving to be a "catch up" year. The United Kingdom is currently trying to save itself at the cost of huge and drastic socio-economic cuts of which student violence, including that against the Royal Family (a rare event), testifies to their unpopularity. But the size of its debt, its financial isolation and the State rescue of its banking debacles (as did Ireland) makes this headlong rush very dangerous, socially, economically and financially. As for the United States, their leaders seem to do everything (by "doing nothing") to ensure that 2011 is truly the year of the "Fall of the Dollar Wall" as LEAP/E2020 anticipated in January 2006. [15] As Liam Halligan pointed out in The Telegraph of 11.12.2010, this development on interest rates does not bode well for US debt, expressing what LEAP/E2020 anticipated over two years ago now: we are reaching the moment of truth when available global savings are insufficient to meet the needs of the West, particularly the gargantuan need of the United States. [16] A factor emphasized by the GEAB team for over four years. [17] European Financial Stabilization Fund, hedge fund regulation, strict limits on bank bonuses, strict regulation of rating agencies, budget monitoring, next reinforcement of the whole of the European internal market financial regulation, first Euroland rating agency, … Sources: European Voice, 26.10.2010; Deutsche Welle, 5.11.2010; Reuters, 13.7.2010; ABBL, 8.12.2010; BaFin, 16.11.2010 [18] Wolfgang Schauble, the German Finance Minister, is currently the only politician who dared to clearly show his colours in his recent interview with Bild magazine, in which he states that during the next ten years, Euroland countries will have accomplished a genuine political integration. Karl Lamers, his colleague in charge of European affairs at the core of the CDU, identifies the crisis as an opportunity for Europe and Germany, as wel as as the too rarely heard American voice of Rex Nutting in the Wall Street Journal of 8.12.2010. On the technocratic side, the ECB President, Jean-Claude Trichet, called for a "budgetary federation" in Euroland. Sources: EUObserver, 13.12.2010; DeutschlandFunk, 9.12.2010; EUObserver, 1.12.2010 [19] For over a decade, public opinion in the Euroland countries has been, in effect, much more "integrationist" than their élite. Thus, rejection of the draft European Constitution in 2005 in France and the Netherlands would not have happened without some "pro-Europeans" voting "No", rejecting a draft that they considered too timid, politically, democratically and socially. [20] European leaders are like the tortoise in the Jean de La Fontaine fable "The Hare and the Tortoise" ... but the race would be described by hares! [21] By the way, the Eurozone’s future political leaders would be well advised to practice, as quickly as possible, how to manage Euroland through two interactive games, Economia and Inflation Island, that the European Central Bank has made available to the public. [22] As LEAP/E2020 has repeated for nearly two years, European austerity is politically viable only if accompanied by unquestionable social and fiscal equity and the implementation of major democratic and social projects throughout Euroland. It is here that the real medium to long term weakness of the Eurozone can be found, not in the sovereign debt of the peripheral countries. To illustrate this point, it is useful to watch the very interesting video coverage made by the New York Times during the summer of 2010, called "The Austerity Zone: Life in the New Europe ". [23] Given the obvious difficulty of the American élite to understand the developments taking place in Europe, LEAP/E2020 wishes to contribute to the debate currently raging on US college campuses where budget austerity has led to heavy cuts in language teaching. As always, behind budgetary justifications, several "hidden agendas" can be identified as well as candid lack of understanding of what's going on in the rest of the world regarding languages. A perfect example of both trends seems to be Richard N. Haas, former key official of the US State Department in the G.W. Bush administration, and now the president of the influential Council of Foreign Relations, who strongly advocates pushing French, German and Russian languages out of US campuses. With such 'enlightened and fair' advisers (qualified as having «an intellectual deficit» to understand the 21st century world at the GlobalEurope seminars in The Hague and Washington in 2004/2005), US students are doomed to be less and less able to understand tomorrow's world. Therefore, LEAP/E2020 finds it timely to circulate its 2007 anticipation entitled 'Which languages will the Europeans speak in 2025?' again. [24] These will be the bonds used by all Euroland countries and other EU member states who wish to participate as the other countries, except the United Kingdom, did in May 2010 for the European Financial Stabilization Fund. [25] Despite the denials of French and German officials, these Eurobonds are on the agenda of all the informal discussions of Euroland leaders. Source: Euroinvestor, 10.12.2010 [26] It is also probable that the rise in strength of the political renewals expected in France from Spring 2012, and perhaps also in Germany at that time, will make these issues real campaign topics from the end of Summer 2011. [27] Liam Halligan, definitely one of the best British watchers of the global crisis, is thus completely right to stress in The Telegraph of 27.11.2010 that Angela Merkel (and other Euroland leaders as well) has every intention of making investors pay for significant share of their Irish and Greek bets. But that will happen in an organized manner, as an effective and forceful strategy which the strong States are used to; not in a panic, in the context of a mini-crisis. [28] And we repeat that, according to our anticipations, they will probably be the political leaders most independent from banking lobby since the 1990s. [29] This will also take place in an organized manner of “forcibly” cutting back the damaged balance sheets of the major European banks. |

(GEAB, December 16, 2010)

(GEAB, December 16, 2010)

Od istog autora

- First half of 2012: Decimation of the Western banks

- The three US crises: Budget, T-Bonds and Dollar

- Get Ready for the Meltdown of the US Treasury Bond Market

- Major Monetary Oil Shock Predicted for late 2011

- 2011 - The ruthless year, at the crossroads of three roads of global chaos

- Financial Crisis and Global Geopolitical Dislocation

- Spring 2011 - Towards a Serious Breakdown of the World Economic System

- World Economic Crisis and Global Geopolitical Dislocation

- The “Eurozone Coup d’Etat”

- The Bank of England battle

Ostali članci u rubrici

- Playing With Fire in Ukraine

- Kosovo as a res extra commercium and the alchemy of colonization

- The Balkans XX years after NATO aggression: the case of the Republic of Srpska – past, present and future

- Iz arhive - Remarks Before the Foreign Affairs Committee of the European Parliament

- Dysfunction in the Balkans - Can the Post-Yugoslav Settlement Survive?

- Serbia’s latest would-be savior is a modernizer, a strongman - or both

- Why the Ukraine Crisis Is the West’s Fault

- The Ghosts of World War I Circle over Ukraine

- Nato's action plan in Ukraine is right out of Dr Strangelove

- Why Yanukovych Said No to Europe

Anketa

Republika Srpska: Stanje i perspektive