.jpg)

| NSPM in English | |||

First half of 2012: Decimation of the Western banks |

|

|

|

| петак, 21. октобар 2011. | |

|

(GEAB, October 17, 2011)

As anticipated by LEAP/E2020, the second half of 2011 is seeing the world continuing its unstoppable descent into global geopolitical dislocation characterized by the convergence of monetary, financial, economic, social, political and strategic crises. After 2010 and early 2011 which has seen the myth of a recovery and exit from the crisis shattered, it's now uncertainty that dominates the States’ decision-making processes just like businesses and individuals, inevitably generating increasing apprehension for the future. The context singularly lends itself: social explosions, political paralysis and / or instability, return to the global recession, fear over banks, currency war, the disappearance of more than ten trillion USD in ghost-assets in three months, widespread lasting and rising unemployment... Besides, it’s this very unhealthy financial environment that will cause the "decimation[1] of Western banks" in the first half of 2012: with their profitability in freefall, balance sheets in disarray, with the disappearance of trillions of USD assets, with states increasingly pushing for strict regulation of their activities,[2] even placing them under public supervision and increasingly hostile public opinion, now the scaffold has been erected and at least 10% of Western banks[3] will have to pass that way in the coming quarters. In this GEAB issue, our team also presents its 2012-2016 "country risk" forecast for 40 States, demonstrating that one can depict the situations and identify strong trends through the current "fog of war".[4] In such a context, this decision-making tool is proving very useful for the individual investor as well as the economic or political decision-maker. Our team also presents the changes in the GEAB $ Index and its recommendations (gold-currencies-real estate), including of course the means to protect oneself from the consequences of the coming "decimation of Western banks". For this GEAB issue, our team has chosen to present an excerpt from the chapter on the decimation of Western banks in the first half of 2012.

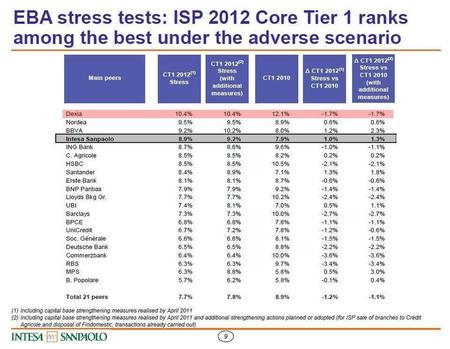

First half of 2012: Decimation of Western banks In fact, it will be a triple decimation[5] culminating in the disappearance of 10% to 20% of Western banks over the next year: - a decimation of their staff - a decimation of their profits - and lastly, a decimation of the number of banks. It will be accompanied, of course, by a drastic reduction in their role and importance in the global economy and directly affect banking institutions in other regions of the world and other financial operators (insurers, pension funds ...). An example of bank information at the time of a global systemic crisis Intesa SanPaulo’s stress test results compared to its European competitors (and compared to the first casualty: Dexia)[6] Our team could address this issue like the Anglo-Saxon media, the president of the United States and his ministries,[7] Washington and Wall Street experts and, on a wider basis, mainstream media,[8] have done recently over all aspects of the global systemic crisis, that’s to say by saying, "It’s Greece and the Euro’s fault!" It would obviously be a virtue to reduce this part of the GEAB to just a few lines and suppress any hint of analysis of the possible causes in the US, the UK or Japan. But, coming as no surprise to our readers, it won’t be LEAP/E2020’s choice.[9] As the only think tank to have anticipated the crisis and rather accurately foreseen its various phases, we’re not now going to give up an anticipation model that works well, benefitting from prejudice without any predictive power (Don’t let’s forget that the Euro is still alive and well[10] and that Euroland has just completed the small feat of, in six weeks, putting together the 17 parliamentary votes needed to strengthen its financial stabilization fund).[11] So, instead of echoing the propaganda or "readymade thought" let’s remain faithful to the method of anticipation and stick to a reality that we must uncover in order to understand it.[12] In this case, for ages, when one thinks of "banks" one thinks first of all of the City of London and Wall Street.[13] And with good reason, London for over two centuries and New York for nearly a century have both been the two hearts of the international financial system and the lairs par excellence of the world’s major bankers. Any global banking crisis (as any major bank event), therefore, begins and ends in these two cities since the modern global financial system is a vast process of incessant wealth recycling (virtual or real) developed by and for these two cities.[14]

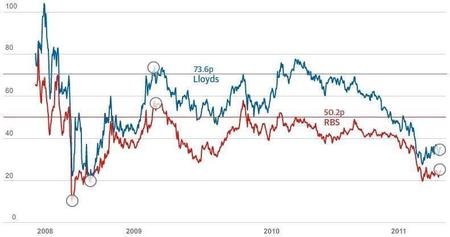

The decimation of the Western banks that begins and will continue in the coming quarters, an event of historic proportions, cannot therefore be understood without first of all measuring and analyzing the role of Wall Street and London in this financial debacle. Greece and the Euro will undoubtedly play a role here as we have discussed in previous GEAB issues, but these are triggers: Greek debt is yesterday’s banking venality that is exploding in the public arena today; the Euro is the arrow of the future that is piercing the current financial balloon. These are the two fingers that highlight the problem, but they aren’t the problem. This is what the wise man knows and the fool doesn’t, to paraphrase the Chinese proverb.[15] In fact, one only needs to look at London and Wall Street to anticipate the future of Western banks, since it's quite simply there that the banking flock gathers together to come and drink its dollar dose every evening. And the condition of the Western banking system can be measured through changes in bank staff numbers, their profitability and their shareholders. From these three factors one can directly deduce their ability to survive or disappear. The decimation of bank staff numbers Let’s begin with the numbers then! Here the picture is bleak for banking sector employees (and now even for the "banking system stars"): since mid-2011 Wall Street and London have continuously announced mass layoffs, spread by the secondary financial centers such as Switzerland and Euroland and Japanese banks. A total of several hundreds of thousands of banking jobs that have disappeared in two waves: first of all in 2008-2009, then since the late spring of this year. And this second wave is gradually gaining momentum as the months go by. With the global recession now under way, the drying up of capital flows to the United States and the United Kingdom as a result of the geopolitical and economic changes under way,[16] the huge financial losses in recent months, and all kinds of regulations which gradually "break" the super-profitable banking and financial model of the 2000s, the heads of major Western banks have no choice: they must, at any price, cut their costs as quickly as possible and deeply. Therefore, the simplest solution (after that of overcharging clients) is to lay off tens of thousands of employees. And that's what is happening. But far from being a controlled process, we see that every six months or so Western bank leaders find that they had underestimated the extent of the problems and are therefore obliged to announce further mass layoffs. With the political and financial “perfect storm” looming in the U.S. for next November and December,[17] LEAP/E2020 anticipates a new series of announcements of this kind from early 2012. The “cost-killers” in the banking sector have some good quarters in front of them when we see that Goldman Sachs, which is also directly affected by this situation, reduced to limiting the number of green plants in its offices to save money.[18] Although, after eradicating the green plants, it’s usually the “pink slips”[19] that flower. The decimation of the number of banks In a way, the Western banking system looks increasingly resembles the Western steel industry of the 1970s. Thus the "ironmasters; thought they were the masters of the world (incidentally actively contributing to the outbreak of World Wars); just like our "major merchant bankers" thought they were God (like Goldman Sachs CEO) or at least masters of the universe. And the steel industry was the "spearhead", the "absolute economic example" of power for decades. Power was counted in tens of millions of tons of steel just like the power of billions in bonuses for merchant bank executives and traders in recent decades. And then, in two decades for the steel industry, in two / three years for the banks,[20] the environment has changed: increased competition, collapsing profits, massive layoffs, loss of political influence, the end of massive subsidies and ultimately nationalization and / or restructuring giving birth to a tiny sector compared to what it was at its heyday.[21] In a sense, therefore, the analogy applies to what awaits the Western banking sector in 2012/2013. Share price changes (and, therefore, losses) for the British taxpayer following the partial government takeover of RBS and Lloyds - Source: Guardian, 10/2011

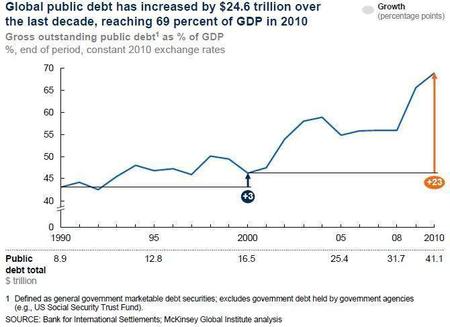

Already on Wall Street in 2008, Goldman Sachs, Morgan Stanley and JP Morgan had to suddenly turn themselves into "bank holding companies" to be saved. In the City, the British government had to nationalize a whole swathe of the country's banking system and to this day the British taxpayer continues to bear the cost because the banks’ share prices have collapsed again in 2011.[22] This is also one of the Western banking system’s characteristics as a whole: these private financial players (or market listed) are worth practically nothing. Their market capitalization has gone up in smoke. Of course this creates an opportunity for nationalization at low cost to the taxpayer from 2012 because it’s the choice that will be imposed on States, in the United States as in Europe or Japan. Whether it be, for example, Bank of America[23], CitiGroup or Morgan Stanley[24] in the United States, RBS[25] or Lloyds in the United Kingdom[26], Société Générale in France, Deutsche Bank[27] in Germany, or UBS[28] in Switzerland[29], some very large institutions "too big to fail" will fail. They will be accompanied by a whole swathe of medium or small banks such as Max Bank which has just filed for bankruptcy in Denmark.[30] Faced with this "decimation", States’ resources will be quickly overrun, especially in these times of austerity, low tax revenues and the political unpopularity of the bank bailout.[31] Political leaders will, therefore, have to focus on protecting the interests of savers[32] and employees (two areas full of electoral promise) instead of safeguarding the interests of bank executives and shareholders (two areas full of electoral pitfalls, whose precedent in 2008 demonstrated its economic futility)).[33] This will result in a new collapse in financial stock prices (including insurance, considered very "close" the banking situation) and increase hedge funds, pension funds[34] and other players’ turmoil traditionally closely intertwined with the Western banking sector. No doubt this will only strengthen the general recessionary environment by limiting loans to the economy just as much.[35] Global public debt (1990-2010) (as a % of GDP, constant 2010 exchange rates) - Sources: BRI / McKinsey, 08/2011 To simplify the view of this development, one can say that the Western banking market, significantly reducing its scope and the number of players in this market, has to downsize proportionally. In some countries, especially those where the very large banks account for 70% or more of the banking market, it will inevitably lead to the disappearance of one or another of these very large players ... whatever their leaders, stress tests or rating agencies say.[36] If you are a shareholder[37] or customer of a bank that may collapse in the first half of 2012 there are, of course, precautions to take. We offer a number in the recommendations in this issue. If one is an officer or employee of such an institution, things are more complicated because we now think it’s too late to avoid serial bankruptcies; and the banking job market is saturated because of massive layoffs. However, here is a piece of advice from our team if you are an employee in any of these institutions, if you are made an interesting offer of voluntary redundancy, take it as the next few months, the redundancies won’t be voluntary and will be under much less favorable conditions. Global Europe Anticipation Bulletin (GEAB) no. 58 [1] Decimation was a Roman military punishment by death of one legionnaire in ten when the army had shown cowardice in battle, disobedience or inappropriate behavior. The Roman system of decimation worked by drawing lots. [2] Regulations that severely excise the banks’ most profitable activities. Source: The Independent, 12/10/2011 [3] Our team believes the percentage to be somewhere between 10% and 20%. [4] Fog of war to which the mainstream media incidentally contribute to a great extent instead of trying to clarify the situation. [5] Considering decimation in its widest sense, that’s to say a sharp decrease can be much more than the Roman era’s 10%. [6] As far as LEAP/E2020 is concerned, this type of classification presages nothing since the current shock is much higher in intensity and duration than the assumptions of the stress tests. And this equally applies to the US banks of course. [7] Taking everything into account regarding Barack Obama, in difficult position for the next presidential elections because of his disastrous economic record and the deep disappointment of most of those who voted for him in 2007 because of his many broken promises, he must at all costs try to blame anyone or anything for the disastrous state of the economy and American society. So why not Greece and the Euro? When that doesn’t work anymore (in a couple of months), it will be necessary to find something else, but short-sighted management is an Obama administration specialty; no doubt his Treasury Secretary Timothy Geithner, the faithful Wall Street link, will find another explanation. In any case, it’s not Wall Street’s fault, we can at least be certain of that. Otherwise, the Obama administration will always bring out the "specter of Iran" to try and divert attention from the United States internal problems. Incidentally, this seems to be the current situation with the cock-and-bull story of the attempted assassination of the Saudi ambassador to Washington by Mexican drug traffickers paid by Iranian intelligence. Even Hollywood would balk at the improbability of such a scenario, but to save the "Wall Street" soldier and try to be re-elected, isn’t it worth a try? Sources: Huffington Post, 26/07/2011; NBC, 13/10/2011 [8] This mainstream media (financial or general) have, in fact, a brilliant history in anticipating the crisis. You certainly remember their 2006 headlines warning you against the 2007subprime crisis, announcing the Wall Street "implosion" of 2008 and, of course, in early 2011 telling you of a major return of the crisis in summer 2011! No, you don’t remember? Don’t worry, your memory is good ... because they never made the headlines, they never warned you of these major events and their causes. So, if you continue to think that, as they repeat every day, the current problems are caused by "Greece and the euro", it’s that you think they have suddenly all become honest, intelligent and insightful ... and you must therefore also believe in Father Christmas in the same sense. It’s beguiling, but not very effective for facing the real world. [9] For a long time, our team has been underlining the European difficulties, anticipating rather correctly the evolution of the crisis on the « Old Continent ». But we try not to fall victim of the syndrom of the European tree that hides the forest of major US and UK problems. [10] A bit of education: those who bet on a Euro collapse a month ago have lost money again. To the rhythm of “the end of the Euro crisis" roughly every 4 months, they won’t have much left by 2012. Whilst the United States for example have not been able to demonstrate their ability to overcome the opposition between Republicans and Democrats on the control of their deficits. [11] Whilst the United States, for example, have not been able to demonstrate their ability to overcome Republican and Democrat opposition on the control of their deficits. [12] It’s appalling to see the G20’s preoccupation with the Euro whilst the central issue of the future is the Dollar. Obviously, the huge media manipulation operation launched by Washington and London will have succeeded once again in deferring, for a time, the inevitable questioning of the US currency’s central status. As anticipated by our team, one can expect nothing from the G20 until the end of 2012. It will continue to talk, pretend to act and to actually ignore the key issues; those are the hardest to put on the table. The recent announcements of an increase in resources for the IMF are a part of these empty words that will not be acted upon because the BRICS (the only ones able to augment IMF funds) will not finance an institution in which they continue to only have marginal influence. Meanwhile, these announcements make believe that there is still a shared commitment to international action. The alarm will be all the more painful in the months to come. [13] If you think of Greece it’s because you are Greek or that you are a manager of shareholder of a bank which has lent too much to the country over the last ten years [14] And in a way also for the two States involved. But this is already a moot point, and widely discussed for that matter, to know if such financial markets are a blessing or a curse for the States and people that host them. [15] “When a finger is pointing at the moon, the fool looks at the finger” [16] Between Euroland’s increasing integration which deprives the City of lucrative markets and closer economic, financial and monetary ties with the BRICS, bypassing Wall Street and the City, they are growing shares of the global financial market escaping London and New York banks. [17] See GEAB N°57 [20] It takes more time to relocate heavy industry than a trader’s desk. [21] This is, more or less, the procedure followed in the United States and Europe. [22] See chart above. [23] Bank of America is definitely at the confluence of major and growing problems: a lawsuit against it claiming $50 billion for concealing losses on the acquisition of Merrill Lynch in late 2008, a massive grassroots rejection by customers following its decision to impose a $5 per month cost for cash cards, a long and unexplained crash of its website; series of trials over subprime involving individual owners and local authorities, and a threat to place Countrywide in bankruptcy, another of its acquisitions in 2008, to limit its losses. According to LEAP/E2020, it embodies the ideal US bank for a crash scenario between November 2011 and June 2012. Sources: New York Times, 27/09/2011; ABC, 30/09/2011; Figaro, 29/06/2011; CNBC, 30/09/2011; Bloomberg, 16/09/2011 [24] The US bank which, in 2008, received the largest slice of public financial support and which, once again, is panicking the markets. Sources: Bloomberg, 30/09/2011; Zerohedge, 04/10/2011 [26] Which itself is also seeing the hour of the cut in its credit rating approach. Source: Telegraph, 12/10/2011 [27] The leading German bank, which is already exposed to a cut in its credit rating. Source: Spiegel, 14/10/2011 [28] UBS is also on the road to a cut in its credit rating. Source: Tribune de Genève, 15/10/2011 [29] Société Générale, Deutsche Bank and UBS have a point in common of particular concern: all three rushed to the US "El Dorado" during the last decade, investing like drunken sailors in the US financial bubble (Deutsche Bank in subprimes, as Société Générale in CDS and UBS in tax evasion). Today, they don’t know how to exit this maelstrom that increasingly drives them to the bottom each day. In passing, we recall that in 2006, we recommended that European financial institutions free themselves from US markets as soon as possible, which appeared very dangerous to us. [30] Source: Copenhagen Post, 10/10/2011 [31] Even the BBC, certainly marked by the UK riots in summer 2011, asks itself a question, "unthinkable" just a year ago for this type of media: can the United States expect social unrest? To ask the question is to answer it. And in Europe, a country like Hungary, with Social-Nationalist government, directly accused the banks, especially foreign ones, of being responsible for the crisis facing the country. Source: BBC, 20/09/2011; New York Times, 29/10/2011 [32] Of which an increasing number have begin to rebel against banking system practices, especially in the United States where Wall Street rejection is growing exponentially, weakening major US banks on a daily basis. Sources: CNNMoney, 11/10/2011; MSNBC, 10/11/2011 [33] And it's even worse than economic futility since a recent study had shown that banks that received public financing were subsequently shown to be the most prone to make risky investments.Source: Huffington Post, 16/09/2011 [34] US public pension funds are now facing a financial chasm estimated at between one and three trillion USD. Will the US public authorities choose to save the banks or their retirees? Because they will soon have to choose. Source: MSNBC, 23/09/2011 [36] None of these banks are able to withstand the global recession and the implosive melding of financial assets that will prevail in the coming months. [37] We could have also developed the point that we are witnessing a process of "bank shareholder decimation". |

The Myth of Economic Recovery

The Myth of Economic Recovery

Од истог аутора

- The three US crises: Budget, T-Bonds and Dollar

- Get Ready for the Meltdown of the US Treasury Bond Market

- Major Monetary Oil Shock Predicted for late 2011

- 2011 - The ruthless year, at the crossroads of three roads of global chaos

- Second half of 2011 - Explosion of the Western public debt bubble

- Financial Crisis and Global Geopolitical Dislocation

- Spring 2011 - Towards a Serious Breakdown of the World Economic System

- World Economic Crisis and Global Geopolitical Dislocation

- The “Eurozone Coup d’Etat”

- The Bank of England battle

Остали чланци у рубрици

- Playing With Fire in Ukraine

- Kosovo as a res extra commercium and the alchemy of colonization

- The Balkans XX years after NATO aggression: the case of the Republic of Srpska – past, present and future

- Из архиве - Remarks Before the Foreign Affairs Committee of the European Parliament

- Dysfunction in the Balkans - Can the Post-Yugoslav Settlement Survive?

- Serbia’s latest would-be savior is a modernizer, a strongman - or both

- Why the Ukraine Crisis Is the West’s Fault

- The Ghosts of World War I Circle over Ukraine

- Nato's action plan in Ukraine is right out of Dr Strangelove

- Why Yanukovych Said No to Europe

Анкета

Република Српска: Стање и перспективе